CFI Newsletter #08: The Price of Extreme Weather

CFI Newsletter #08: The Price of Extreme Weather

+ India's solar troubles (again), a green hydrogen future for India, climate smart credit ratings, and the climate cost of feeding the world

The Climate Finance Initiative Newsletter offers quick digests and insights around what is happening in climate finance. While the Climate Finance Initiative’s current focus of work is India-centric, we will capture a global perspective of climate finance in this newsletter on a fortnightly basis.

March seems to be a spirit of delays. The Ever Given container ship had been stuck for a week until Monday afternoon delaying all transport through the Suez Canal and leading to potential global economic losses anywhere between US$ 6 billion to US$ 60 billion.

We, at CFI HQ, were more distracted than delayed. We did start the month planning to send you a mid-March newsletter edition, as well as the second report of our 4 part series on Strengthening India’s Climate Financing Structure. The next one we are writing focuses on early-stage climate innovation: the current scenario, the gaps, and a couple of fixes to strengthen it.

Now actionable agenda items always come before research at CFI and our distractions this month have been something we plan to share with you soon: some exciting and very promising discussions we are having to start pilots of the financing structures we keep talking about. We will be back with more news on that, and with our next report in a couple of weeks.

To make it up to you, we have added a couple of additional data points to an already power-packed Climate Finance by Numbers this March.

Also, we have been tinkering with calculating the emission savings from all 369 vessels that were parked and waiting to go through the Suez Canal which we’ll try and put in the next edition. If you do come across any sort of math that does the work for us, we will be very grateful :)

Climate Finance by the Numbers

US$ 84 billion

The amount of debt at Indian financial institutions that is at risk from extreme weather events

There is a lot about this number to unpack that gives a fascinating look on how Indian financial institutions are accounting for and viewing climate risks.

This is likely the first time financial institutions in India have disclosed such quantified climate risks, as part of the Carbon Disclosure Project (CDP) disclosure framework for 2020. A lot of the CDP’s work is driving and supporting investors to demand more transparency and action from companies around climate change. These disclosures are indicative of banks and other financial institutions becoming more aware of meeting such investor and public demand.

Speaking of investor demand, The State Bank of India, the bank with the largest climate risk of around US$ 52 billion, acknowledged the potential reputation risks from investors and the wider public around lending to environmentally sensitive projects, which can include climate-intensive activities such as cement, coal, oil and power. These sectors were flagged by the banks as climate exposure risks, which is a step in the right direction towards admitting these sectors’ role in climate change impact, but more steps of restricting financing towards such projects remain to be seen.

Risks from the effects of cyclones, floods, and droughts mainly on the agriculture and food sectors are fairly ubiquitous - the Reserve Bank of India did flag this in their 2019-20 Annual Report - but HDFC did also include an interesting aspect on compensation it would have to pay to employees in case of flooding, which goes beyond the usual scope of climate risk.

Disclosures like these are a step towards getting financial institutions to start thinking about reducing their exposure to climate intensive industries and backing ones that are more supportive of climate action; and financial institutions are very influential in addressing climate risks.

Of the top 67 Indian companies who responded to the CDP disclosures in 2020 - which included a fair amount of climate-intensive businesses - the US$ 84 billion of climate exposure risks disclosed by financial institutions accounted for 87% of the total climate exposure risks reported.

40% and 25%

In keeping with India’s broader mandate to encourage domestic manufacturing, solar modules imported from China and elsewhere have been slapped with an import duty. But as Shravan’s grandfather used to say, one swallow does not make a summer. Likewise, one tariff action is not likely to lead to a boom in solar panel manufacturing in India.

For one, the duty itself may not be enough to make imported solar panels unviable. The price disparity will obviously reduce. The BCD will make imported solar modules 6% - 8% more expensive than domestic manufactured ones, from today’s scenario where imports are almost 25% cheaper. However, the cost of modules made using imported solar cells is likely to still be about 4% to 5% cheaper, even with the BCD.

Then there is the sheer scale of our solar panel imports. Solar module and solar cell imports today account for almost 80 to 90% of the overall demand in the country. The improved economics would incentivize more domestic manufacturers, but the current capacity of 2.5 GW for solar cells and 9 GW for solar modules is insufficient to meet our needed demand.

Developers also argue that imported products are technologically better, largely due to the backward integration these manufacturers have that influence the raw materials and smaller components they use. Concrete incentives for manufacturing around R&D and commercial support, especially around backward integration, needs to be encouraged which tariffs do not address.

A more pressing concern, however, is that this comes at the end of a long series of policy disruptions we have seen in the solar sector in the past year. The story of India’s policy directions around renewable energy is built around such one-off approaches, that often end up being in conflict with one another, rather than being a structured and cohesive approach. For instance, how does having the largest coal mine auction ever just last week, and restricting net-metering for the already flagging rooftop solar to be less viable, fit with catching up to a lagging renewables target that is stated to be a main goal for the country?

The tariff comes into effect for already bid projects that are expected to go live post-April 2022. Costs are going to increase to consumers and discoms from next year at least, with power purchase costs projected to increase by at least US$ 120 million in the coming years.

We are already on track to not achieve the 100 GW target by end 2022 - we are at just 39 GW right now - and this project cost increase will likely reduce the trajectory further. Policy signals are important to encourage more investments in solar adoption. The lack of consistency that India has shown can affect the mid-to-long term solar deployment.

3

The number of green hydrogen partnerships set up in India this year

The number might be a bit of a stretch to be a power-packed metric but we have to talk about green hydrogen and its potential in India.

The partnerships towards producing green hydrogen in India - BGR Energy Systems and Portugal’s Fusion Fuel Green, Indian Oil and Greenstat Norway, and Acme Solar Holiding and France’s Lhyfe Labs - all in the past 2 months, build on moves to make green hydrogen the next big frontier in the Indian cleantech space; a National Hydrogen Energy Mission has been mooted by both the Prime Minister and Finance Minister to be set up in the upcoming year.

But what are the prospects for green hydrogen exactly?

The Energy and Resources Institute (TERI) projects that hydrogen demand in India will increase to 28 million tons per year by 2050, from the current 6 million tonnes, on the back of increased use in ammonia production, in reducing the amount of coal in the steel industry, and in being used as a fuel source in transport and industry.

Almost all hydrogen today is created as a by-product from fossil fuel sources, with around 9 tons of carbon dioxide emissions generated for 1 ton of hydrogen produced. Green hydrogen focuses on production through renewable sources which eliminate the GHG footprint in production at least.

There is a big caveat to this rosy future gazing: producing 1 kg of hydrogen requires 50 kWh of electricity. TERI’s report covers this in-depth, but the energy-intensive nature makes grid energy the most feasible form of energy input for hydrogen production. For the grid to be green, India’s needs to meet its renewable energy targets. The 2022 target of 175 GW renewable energy installed, at least, is unlikely to be met (see No. 3 of this edition’s Climate Finance by Numbers).

We do not think we should discount captive renewable energy setups, like the demonstration facility BGR Systems and Fusion Fuel Green are looking to set up in Tamil Nadu, at this early stage. It is a start and we should be hopeful that these partnerships and a wider policy stance provide the impetus to get green hydrogen to commercialisation. TERI takes a positive outlook at least: by 2050, it projects that nearly 80% of India’s hydrogen will be green.

3 and 5

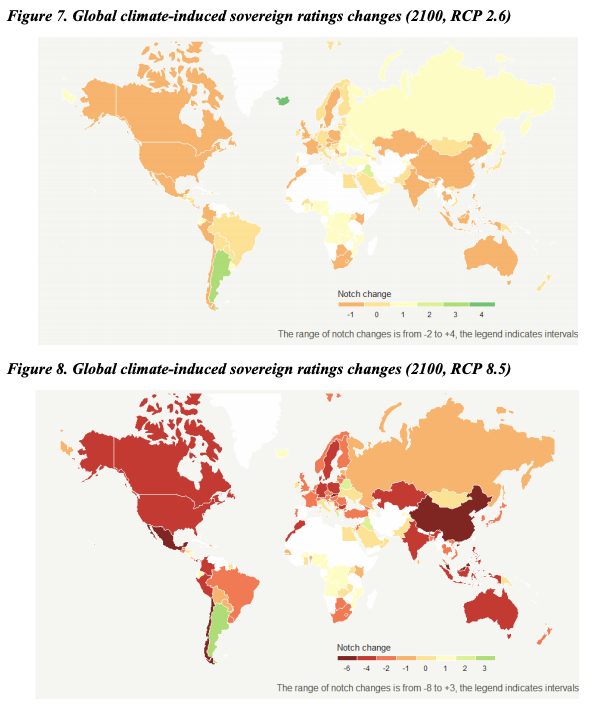

In a report with many eye-popping numbers, we have gone with an admittedly click-baity one that reflects a high emissions scenario where limited greenhouse gases are curbed leading to a 5°C increase in global temperatures by 2100. (This surely cannot happen, can it?)

We have not so far paid much heed to how climate change will reflect in credit ratings and cost of capital for countries. A report by The Bennet Institute for Public Policy from Cambridge does just that. It simulated the economic effects of climate change on Standard and Poor’s (S&P) ratings for 108 countries over the next ten, thirty and fifty years, and by the end of the century. The report is likely the first projection of “climate-smart” credit sovereign ratings. (We highlighted India as CFI is a mainly Indian-centric platform, but it does not make good reading for almost all countries surveyed.)

The report makes three compelling points:

Markets need credible information on how climate change translates into material risk

Greater knowledge of such climate risks by markets is what will lead to these downgrades occurring

Most current ESG ratings and corporate disclosures are unregulated and detached from science and do not do enough to inform markets of climate risks. (As an aside, The CDP follows the Science Based Targets Initiative in guiding their disclosure framework.)

RCP 2.6 refers to a ‘stringent climate policy’ scenario consistent with limiting warming to below 2°C. RCP 8.5 is a high emissions scenario with limited greenhouse gas curbed consistent with a 5°C warming world. No matter the outcome, climate change is going to affect the cost of sovereign and corporate debt borrowing:

Under the stringent climate policy scenario of RCP 2.6, additional costs of global sovereign and corporate debt due to climate risk downgrades is expected to be between US$ 29.2 - 45.6 billion.

Under the high emission scenario of RCP 8.5, additional costs of global sovereign and corporate debt explode and is expected to be between US$ 172.8 - 267.6 billion.

The report is a first in accounting for climate risks in credit ratings. It positions itself as a step in bridging the gap in translating climate science into credible risk metrics for financial decision-makers, which today’s ESG metrics do not do. It quite likely should be a wake-up call for countries to be more aware of the financial consequence of their climate action or the lack of it, and for ESG platforms to better inform on this.

US$ 26.4 billion

The climate cost of food and agriculture tends to be muted in the public eye, except for the visible annual spells when large swathes of the Amazon are set ablaze as part of deforestation drives for grazing cattle, and planting soy and other crops.

We, at CFI HQ, believe that this is one cost that we should look at more keenly.

There is an overriding challenge, and opportunity, of having to feed 10 billion people by 2050, 3 billion more than our current numbers. When looked at through a climate impact lens, the stats around the nexus of agriculture-deforestation-greenhouse emissions are extensive, and we will only lecture you with three top ones:

Agriculture and deforestation are responsible for nearly a quarter of global greenhouse gas emissions.

By 2030, livestock production is projected to consume nearly half the world’s carbon budget - the carbon emission limit we should live within to not miss emission targets (which we in effect do not).

Agriculture is the biggest driver of deforestation globally, responsible for half of all recent tree loss and more than 90 percent tree loss in the tropics.

Palm oil, soy and cattle are the largest commodities behind this loss, with cattle accounting for more than half. With a $26.4 billion investment, financial institutions are going some way to combat the consequent climate impacts. Food, however, is not as straightforward to create a shift in as it might be for energy to move away from fossil fuels. Demand is fuelled by lifestyle and culture, among others, which is a lot more intrinsic and important to individuals and communities than the greenhouse gas emissions associated with them.

The Net Zero Asset Owner Alliance is one example of these challenges. Earlier this week, the Alliance saw 43 more asset owners sign up to the commitment of having net-zero portfolios through the investments by 2050. However, these included Blackrock and Vanguard, who also happen to be the largest shareholders of JP Morgan which has invested over US$ 1 billion in food-related forest-risk commodities since 2016, including Brazilian meatpackers who have contributed to the deforestation of the Amazon.

Certainly, the deforestation linked to agricultural commodities has to be curtailed sooner rather than later, and this perhaps is the overdue start that financial institutions can be compelled to target.

Engaging with CFI

As always, if you are keen to engage or talk to us on our work plans (check out the deck here) or if you have something of your own to collaborate on, reach out to us below!

That’s it for Edition #8 of our newsletter.

As always, send all feedback, compliments and brickbats our way. And of course, we do appreciate you spreading the word about this newsletter.

Best,

Simmi Sareen and Shravan Shankar